The road to financing a project is not always a straight, simple one. In many cases, there is a combination of factors, such as the timing of investments, availability of resources, and unforeseen complications that can get in the way of simply having a project and seeing it to completion.

Financing is definitely one of those areas where things get tricky. But for people in business that are willing to do their research and consider somewhat less traditional alternatives, there are ways to get around some financial hurdles. The bridge loan is one of these things, but how does it work?

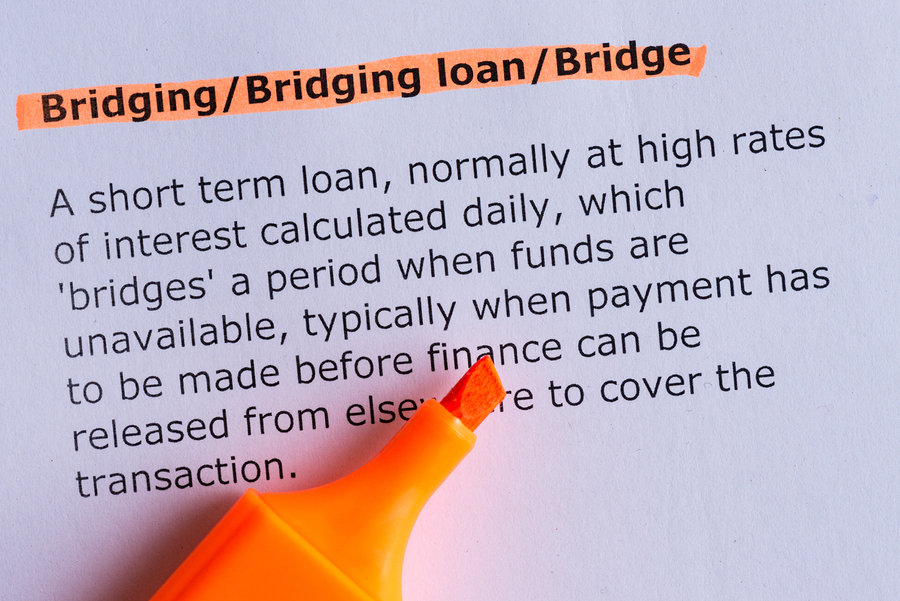

The Stopgap Measure

The name says it all, a bridge loan is often a short term loan that may be used to cover certain costs until the desired, long term funding is available. In private residential terms, this might be a loan that an owner would take if there’s an interest in buying a new home, while still trying to sell the current home. The bridge loan would cover the cost of initial down payments and other associated costs with the purchase of a new home. Once the current home is sold, part of the profits from that sale then go towards paying off the initial bridge loan that made the purchase possible in the first place.

In real estate development, there are many such situations where bridge loans play a similar role. However, terms and conditions tend to be more stringent for these loans, especially on projects where there is no guarantee that it will even be approved and moved forward. Bridge loans in situations like this can “get the ball rolling,” allowing investors to start up a project and get the manpower and equipment available to start work until such time as a construction loan or other form of borrowing comes through.

A bridge loan involves a bit more risk, but if you plan your finances well, and ensure that your project is a very promising one, bridge loans can often be a useful tool to start an otherwise difficult project.