How to Calculate DSCR (Debt Service Coverage Ratio)

Understanding how to calculate DSCR is essential for real estate investors,

lenders, and borrowers evaluating loan eligibility and cash flow strength.

The debt service coverage ratio (DSCR) measures how easily a property’s income

covers its annual debt obligations.

In this guide, we break down the debt service coverage ratio formula,

show step-by-step examples, and explain what lenders look for when

calculating DSCR.

What Is Debt Service Coverage Ratio (DSCR)?

The debt service coverage ratio is a financial metric used by lenders to

determine whether a property or business generates enough income to cover its debt payments.

DSCR compares net operating income (NOI) to total annual debt service,

including principal and interest payments. It is one of the most important ratios

used in commercial and investment property lending.

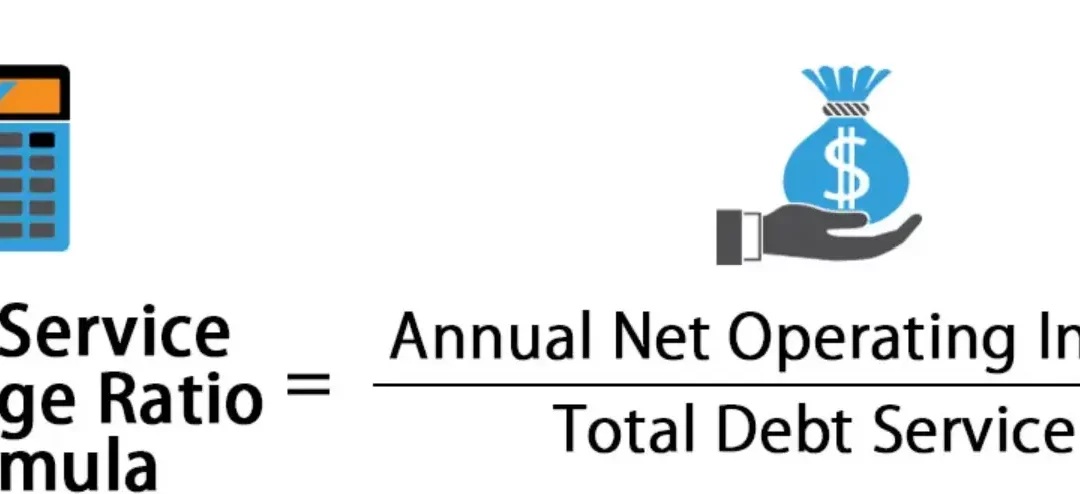

Debt Service Coverage Ratio Formula

The standard debt service coverage ratio formula is:

DSCR = Net Operating Income ÷ Total Debt Service

- Net Operating Income (NOI) = Rental income minus operating expenses

- Total Debt Service = Annual principal + interest payments

This same formula may also be referred to as the

debt coverage ratio formula, depending on the lender.

How to Calculate DSCR Step by Step

- Determine the property’s annual gross rental income

- Subtract operating expenses to calculate net operating income (NOI)

- Add up total annual debt payments (principal + interest)

- Divide NOI by total debt service

This step-by-step process ensures accurate and lender-approved

calculating DSCR results.

DSCR Calculation Example

Let’s look at a real-world example:

- Annual rental income: $120,000

- Operating expenses: $40,000

- Net Operating Income (NOI): $80,000

- Annual debt service: $65,000

DSCR = $80,000 ÷ $65,000 = 1.23

A DSCR of 1.23 means the property generates 23% more income

than required to cover its debt obligations.

What Is a Good DSCR?

Most lenders use the following DSCR benchmarks:

- 1.00 – Break-even (higher risk)

- 1.15 – 1.25 – Minimum for many DSCR loans

- 1.30+ – Strong cash flow and lower risk

The higher the DSCR, the easier it is to qualify for favorable loan terms.

Common Mistakes When Calculating DSCR

- Using gross income instead of net operating income

- Excluding vacancy or maintenance expenses

- Ignoring escrowed taxes and insurance

- Using monthly instead of annual figures

DSCR Frequently Asked Questions

Is debt coverage ratio the same as DSCR?

Yes. The terms debt coverage ratio and

debt service coverage ratio are often used interchangeably by lenders.

Do DSCR loans require personal income verification?

Many DSCR loans focus primarily on property cash flow rather than borrower income.

Can DSCR be calculated using Excel?

Yes. Most investors use Excel or Google Sheets when calculating DSCR for multiple properties.

Using DSCR to Qualify for Investment Property Loans

DSCR plays a major role in determining eligibility for investment property financing.

If your property meets DSCR requirements, you may qualify without traditional income documentation.